Background

On April 11, 2020, Bill C-14: A second Act respecting certain measures in response to COVID-19, received Royal Assent. As part of Bill C-14, The Canada Emergency Wage Subsidy (the “CEWS”) was enacted.

The purpose of the CEWS program was outlined in a Government of Canada/CRA online bulletin entitled “Benefits, credits and support payments: CRA and COVID-19”, which states:

As a Canadian employer whose business has been affected by COVID-19, you may be eligible for a subsidy of 75% of employee wages for up to 12 weeks, retroactive from March 15, 2020, to June 6, 2020. This wage subsidy will enable you to rehire workers previously laid off as a result of COVID-19, help prevent further job losses, and better position you to resume normal operations following the crisis. Starting April 27, 2020, eligible employers can apply in CRA My Business Account or through a separate online application form.

Since the CEWS program will allow employers to recover certain amounts paid to employees, it is hoped that the CEWS program will motivate employers to pay employees at least 75% of their previous wages.

Although the rules and calculations are complex, in order to qualify for the CEWS you must be an ‘eligible employer’ and be paying ‘eligible employees’ amounts considered to be ‘eligible remuneration’, as discussed below.

Eligible Employers

The CEWS will be available to most employers, regardless of size, including individuals, taxable corporations, partnerships (consisting of eligible employers), trusts, registered charities and certain other tax-exempt entities.

The CEWS is not available to public sector entities including hospitals, schools, public universities, municipalities and local governments.

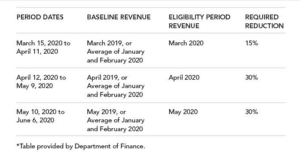

To qualify for the CEWS, an eligible employer must experience a reduction in their ‘qualifying revenue’ as follows:

March 2020: 15% reduction

April 2020: 30% reduction

May 2020: 30% reduction

The calculation of ‘qualifying revenue’ is complex, but the reduction in qualifying revenue can essentially be determined either by reference to the revenue earned in the corresponding month of 2019, or the average of the revenue earned in January and February of 2020, as illustrated by the following table:

Eligible Employees

For the purposes of the CEWS, an ‘eligible employee’ is essentially defined as an individual who is employed in Canada by the employer during the applicable claim period, unless during a period of 14 or more consecutive days during the applicable claim period the employee did not receive remuneration from the employer.

An eligible employee can receive retroactive eligibility if they have been laid off or furloughed as long as they are rehired by the employer and their retroactive status and remuneration meet the eligibility criteria for the applicable claim period. In order be included in the calculation for the subsidy, the eligible employee must first be rehired and paid.

Eligible Remuneration

The subsidy is based on the amount of eligible remuneration paid to an eligible employee.

Eligible remuneration includes amounts paid by an eligible employer to an eligible employee as wages, salaries, commissions, fees, and other taxable benefits. Generally, it is amounts paid to an employee that normally attract withholding and remittances obligations to the CRA.

Calculation of Subsidy

Although the calculation of the subsidy is complex, the amount of the subsidy for an employer paying remuneration to an employee between March 15 and June 6, 2020 is essentially the greater of:

(i) 75% of the amount of remuneration paid, up to a maximum benefit of $847 per week; and

(ii) the amount of remuneration paid, up to a maximum benefit of $847 per week or 75% of the employee’s baseline remuneration, whichever is less.

Penalties

If an employer enters into transactions to artificially reduce revenue in order to claim the CEWS, the employer would be required to repay the full subsidy that was claimed. The employer would also be subject to a penalty equal to 25% of the total value of the subsidy. In addition, fraudulent claims may attract additional penalties including fines and possible imprisonment. In order to avoid employers manipulating or abusing the CEWS program, specific anti-avoidance rules have also been included in the legislation.

Conclusion

The CEWS program can provide significant benefits to both employers and employees during this difficult time by cushioning the impact of substantial reductions in revenue and the corresponding impact it has on employment. However, the qualification and application process for the CEWS program, and the corresponding calculation of the subsidy itself, are intricate and complex. If you require assistance navigating the CEWS program or determining eligibility for the subsidy itself, we would be happy to assist you.

The above discussion is only a generalized summary of the CEWS program and is not meant to be viewed as a detailed discussion of all the rules, requirements, and benefits of the program.

Please do not hesitate to contact us, your relationship partner or lawyer if you have any questions or if we can be of assistance in guiding you through these new challenges.

This article was prepared by:

MICHAEL A. SELCHEN

PARTNER

204.956.3577

[email protected]

This article represents general information and is not legal advice. Please contact us if you would like legal advice that is tailored to your particular circumstances. We would be happy to help.